Michelin Guide Debates II

Food production and distribution systems have always stood at the very center of the drive for profit, and it is hard to deny that monopolization began almost from day one.

Yet the restaurant sector, which forms the final external link of the food system, survived across Europe largely as small-scale businesses until the last quarter of the twentieth century.

From the field to the table, whether at home or outside, food supply has been reshaped over the last fifty years above all by monopolization. Farmers, local producers, and neighborhood grocers have gradually given way to agribusiness, to a food industry dominated by global brands, to wholesale markets, and to fast food chains. This transformation is now almost complete.

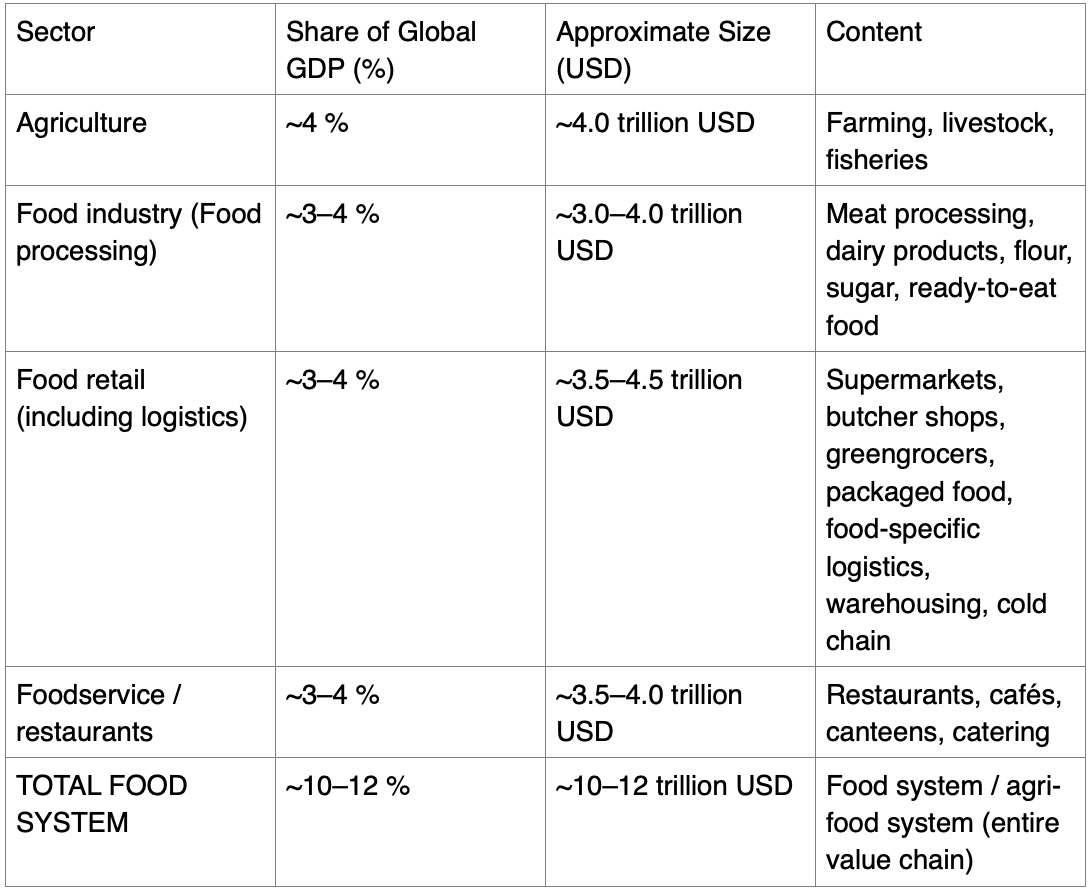

A food service sector generating three to four trillion dollars

As home cooking has been almost entirely commodified through prepared and processed food, the final delivery layer known as Food Service, which includes all forms of eating outside the home, has increasingly been drawn directly into the agrifood system through supply networks. Independent restaurants, in a reductive sense, have been compelled into this integration.

Today the commercial scale of food consumed outside the home is comparable to agriculture itself, to food processing, and to food retail within global GDP. As shown in Table 1, each of these sectors has a volume of roughly 3.5 to 4.0 trillion dollars. Taken together, the agrifood system represents around 10 to 12 trillion dollars, roughly 10 to 12 percent of the world economy.

Table 1. Global GDP Share – Food System

*Global nominal GDP is assumed to be approximately 100–105 trillion USD.

*Values are approximate and indicative.

*Figures are given using the value-added approach.

*Food-specific logistics, storage, and cold chain costs are included under food retail.

*These figures are approximate estimates based on value added, assuming a global nominal GDP of around *100 to 105 trillion dollars. Food specific logistics and cold chain costs are included under food retail.

Agriculture accounts for about 4 percent of global GDP, roughly 4 trillion dollars, including farming, livestock, and fisheries.

Food processing represents around 3 to 4 percent, approximately 3 to 4 trillion dollars, covering meat, dairy, flour, sugar, and processed foods.

Food retail, including logistics, accounts for about 3 to 4 percent, roughly 3.5 to 4.5 trillion dollars, including supermarkets, butchers, greengrocers, packaged food, storage, and cold chains.

Food service and restaurants also represent about 3 to 4 percent, around 3.5 to 4.0 trillion dollars, covering restaurants, cafés, canteens, and catering.

The total food system thus reaches roughly 10 to 12 percent of global GDP.

Chain restaurants versus independent restaurants

Although chain restaurants first emerged in the United States in the 1920s with promises of hygiene, low prices, and standardized service, they only reached significant economic scale in the final quarter of the twentieth century. Today chains account for roughly 30 percent of the total food service market.

In Europe, nearly twenty to twenty-five years passed between the opening of the first McDonald’s outlets in the 1970s and the full establishment of chain restaurants across the continent. Despite this, food service is still largely dominated by independent family businesses, mon-and-pop restaurants, small investors, micro scale companies, and chef owned establishments.

Globally, a large share of these independent businesses, representing six to eight trillion dollars, no longer source primarily from local suppliers. Instead, they purchase mostly from global suppliers that dominate markets, set prices and payment terms, and control production from seed to shelf.

Although chains already occupy about 30 percent of the market, the remaining large share is expected to undergo ownership changes and new forms of control over the coming decades. Neighborhood gathering places, workers’ lunch restaurants, tourist establishments in city centers, and even restaurants celebrated in guides for their gastronomic value will increasingly become dependent on supply chains that control agriculture, food processing, and retail distribution from the ground up.

One leg of this transformation is finance. The other is marketing. Close to the center of this marketing network stand guides that rate, recommend, and elevate restaurants, often tied to the same supply chains through sponsorship mechanisms.

What lies ahead for independent restaurants?

There was a time when well loved restaurants allowed beverage brands to display their names on the awnings outside their doors. That awning was an extension of the restaurant. By carrying a beer or soda brand, the restaurant was saying to the customer: you can drink this here, I trust this product, you can buy it. In short, the restaurant was the reference point for the consumer.

Today, after fifty years of transformation, the logic has reversed. The restaurant has become an extension of the global beverage monopoly. The supplier, whose name appears on the awning, now effectively says: you will consume my product here.

Survival increasingly depends on being supported by a beer brand, endorsed by a soft drink company, or included in guides. Behind these recommendation platforms stand a shrinking number of food and beverage monopolies acting as sponsors.

Before the seed even touches the soil, the production process begins. At its final link, a wholesale delivery truck pulls up to the restaurant door. Invoices are issued on credit. The restaurant that once served as a meeting point for neighbors, workers, shopkeepers, white collar employees, and families is now dependent on the very conglomerate whose brand it once promoted. It mostly reheats, plates, or finishes cooking products that have already been processed. Only a small fraction is truly cooked from scratch. When the customer pays the bill, the money often flows directly upward to the supplier monopoly.

After fast food chains, the second stage has being the integration of neighborhood restaurants, industrial zone eateries, city center staples, and tourist favorites into monopolized supply chains. Ownership change is not essential. Restaurant owners increasingly resemble self employed subcontractors. What matters is that restaurants are becoming the final delivery points of supply chains, the interface with the end user. This process is rapidly reaching completion.

Will the restaurants listed by the guides be the final link in the supply chain?

Now it is the turn of the upper layer of food service. Restaurants offering gastronomic value, frequented by the middle and upper middle classes and even preferred by the upper class, are next in line.

Starred guides and popular recommendation platforms have therefore gained growing importance and reach. In this model, the chef and restaurant that apply the final touch to the plate are absorbed into the network. Even starred restaurants are reduced to the last link in a closed system, transformed into plating stations where profit is realized. This trend is spreading quickly.

In summary, the share of farmers and local producers in agriculture, including livestock and fisheries, has shrunk dramatically not only in the West but also in late industrializing and poorer countries. Giant corporations such as the ABCD group control more than 60 to 70 percent of global agriculture. Food processing has long been monopolized, from pasta to tomato paste. Retail distribution followed the same path, as small grocers vanished and supermarkets gave way to chains and wholesale markets.

What remains relatively unabsorbed is food service and local independent restaurants, still about 70 percent of the sector. Their turn for integration has arrived.

Yet for many restaurants, openly appearing as a chain link would destroy their symbolic value. This is where new models and guides step in, turning independent restaurants into links in the food chain while concealing the system behind linen tablecloths and absorbing all added value.

Welcome to the era in which famous chefs and talented cooks are once again becoming serfs.

A concrete example

Suppose you visit a restaurant recommended by a guide you follow. Thankfully, you were not pushed there by social media influencers. Guides are surely more objective, right?

- You make a reservation and walk through the door. Who are you in this setting? How should we define you?

- You are the final user in the food supply process.

- You pay the bill and thus purchase all the goods and services embodied in the plate before you. But whose customer are you really? Only the restaurant’s?

- Or also the monopolies that control 90 percent of global grain production and trade, whose barley was grown on their farms or contract fields, processed in ever fewer but ever larger factories, distributed through familiar retail chains, and finally delivered to your table?

- The waiter merely opens the bottle and pours the beer. The money, of course, flows upward. The same applies to the food on your plate.

The restaurant is now only the final stage of the supply process. It cooks and plates goods that are already processed to varying degrees. The tomatoes, parsley, fresh pasta, and flour delivered to the kitchen have already undergone harvesting, sorting, packaging, and long transport. Ask yourself: how many grams of diesel fuel are embodied in that sprig of parsley? How much in the butter, the chop?

What is new and critical is this: whether you buy ingredients to cook at home or eat a plated dish at a restaurant, you consume products from the same supply chain. Restaurants no longer generate most of the value. The profit realized at this final stage no longer accumulates there but is absorbed by suppliers. A small portion is then spent on marketing to direct customers to particular restaurants loyal to the chain.

The function of guides

This is where guides enter the picture. These respectable and supposedly neutral recommendation mechanisms, together with social media, displace the role of taste in attracting customers. New communication tools make this effective and popular, while traditional word of mouth fades away. Is it possible for a restaurant to receive a recommendation in the guide only three months after its opening? “The fact that a restaurant can enter the guides only three months after opening demonstrates that the long-standing assessment process based on stability and proven merit has been entirely replaced by a marketing-driven certification system.

What attracts customers is no longer the restaurant’s added value, its pantry transformed into flavor, but a recommendation system shaped by sponsorship networks. Global water brands, the largest soft drink companies, tonic and beer brands, and wholesale suppliers sponsor these guides. We understand why.

Because, survival is difficult even with such support.

This model now invades even starred restaurants… What about taste? As restaurants rely more on industrial products, small producers lose customers and artisanal goods disappear. Dependence on supermarkets and wholesale markets deepens.

Is a creative cuisine possible when captive to suppliers?

Let us ask again: what happens to taste? And what about traditional cuisine?

When local suppliers vanish and suitable ingredients disappear, traditional cuisine follows. You cook what your supply chain and financiers provide. Instead of flavors rooted in tradition, you are pushed toward a so called creative cuisine that relies on standardized ingredients and emphasizes presentation over taste. Creativity becomes less a choice than a necessity.

Along with small farmers, herders, and fishers, dishes and flavors die out. Soon, perhaps within a generation, chefs who have never tasted real vegetables will cook for customers who have never known them.

The working class has long been condemned to industrial food and life. Eating out for them has meant fast food chains for decades, and only rarely. Now even the middle class and lower segments of the upper class can hardly escape this monopolized supply order. After all, even starred restaurants can earn stars by reheating wholesale baklava and serving it with a flourish, can they not?